Business Models Reflect Operator IoT Development

I. Operator Challenges and Solutions in the Flourishing Era of IoT

An exciting future is just around the corner for the Internet of Things (IoT)! As indicated in Vodafone IoT Barometer 2017/18, 2017 is a fantastic year for IoT. The number of enterprises engaging in large-scale IoT deployment (over 50,000 connected devices) has doubled since 2016, quickly growing as a widely recognized key to future business success.

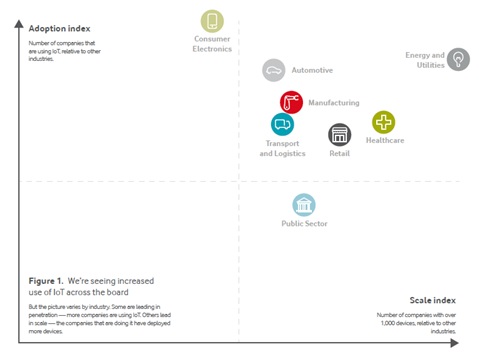

Figure 1: Increased use of IoT across various industries (source: Vodafone IoT Barometer 2017/18)

Healthcare, transport and logistics, energy and utilities, and Internet of Vehicles (IoV) are the major fields that have extensively and vigorously adopted IoT.

Healthcare :

The number of advocates that have largely embraced IoT on a massive scale has noticeably increased over the past months. 86% of all healthcare enterprise adopting IoT have deployed more than 1000 IoT devices. IoT-assisted healthcare has come a long way since proof of concepts and trials. It is now exhibiting unique advantages in cost saving and operational efficiency improvement after triumphing over long-standing barriers in market fragmentation, funding and depreciation, and regulation.

Transport and logistics :

Cost saving and efficiency improvement are the primary objectives in transport and logistics. 52% of transport and logistics companies are seeing reduced costs, and 50% consider IoT as the primary driving force for their business transformation and definitive tool for optimizing asset and resource utilization. 78% believe that network coverage is of superlative importance and bears higher priority than security.

Energy and utilities :

This industry is considered to be one of the top three criteria in terms of adoption. 84% of adopters say that their use of IoT solutions has grown over the past 12 months. 51% are using IoT to improve and automate existing processes. 40% believes that IoT has increased their ability to comply with regulatory and legislative requirements. The uncertainty of this industry adopting IoT stems from the disruption of existing interest and benefit landscapes. The historical business models shall be replaced by new alternatives. This means that utility companies are either vertically integrated or have to work more closely with partners to deliver services to consumers.

IoV: This industry is top listed in consideration of IoT adoption at scale. It has become increasingly difficult for vehicle manufacturers to differentiate their products in terms of performance, reliability, and price. 51% of vehicle enterprises believe that IoT has vastly improved their product competitiveness and successfully created new sources of prospective revenue. 16% have 10,000 or more connected devices.

Operators Challenges

During the past two decades, telecom operators have been pursuing more services and connecting people. It is commendable that they have achieved admirable advances in a relatively short period of time, as mobile phones have a penetration rate of almost 100% among adults. Facing the infatuated 2C market that will hardly benefit from population dividends, telecom operators are seeking for opportunities in the B2B market, hoping to increase the proportion of revenues from ICT industries. As a growing trend, operators are shifting their focus from connecting people to connecting things.

As an ancient Chinese poem goes, "coming events cast their shadows before them." Telecom operators have already sensed the upcoming challenges that IoT has cast before them. They must escape from the limitations of being a sole pipeline provider, seek for high-value customers and applications across the fragmented industries, introduce the IoT platform to more diverse industries, and discover solutions to a multitude of other imminent issues.

Value of IoT Connections Never Lying in Pipelines

All telecom operators must firstly decide whether to be a pipeline provider or a service provider? This is a question that commands a great deal of thought and consideration. Industries typically show their cost concerns by constantly selecting the least expensive connection solution, without much regard for applied technology. The number of cellular connections borne on operator networks accounts for approximately 10% of the total IoT connections. The majority of the IoT connections are based on ZigBee, Bluetooth, Wi-Fi, and cabled networks. Revenues from IoT cards accounts for only 10% of those from traditional individual services, and the value of pipelines occupies as little as 2% within the entire IoT industry chain. A number of gas and water companies have even stated that they are not willing to pay more than 0.9 USD for communications on each connected meter per year.

Scenario Fragmentation Impeding Solution Incubation

The IoT industries are extended and diversified, and therefore lack the benefits that are associated with economies of scale. Application incubation requires deepened integration with each industry and their related manufacturing and business processes. Telecom operators must equip themselves with expertise of verticals and specialists who fully understand the verticals before they can be a reliable enabler. Operators must ensure they are making correct decisions concerning industry selection to realize large-scale IoT applications and embrace IoT for abstracting individual demands as common industry requirements. However, the process of arriving at unequivocal decisions is by no means easy.

IoT Platform for Industries. Enabler or Inhibitor?

In order to transition from M2M to IoT, operators must establish an IoT platform as a critical enabler for all the connections in a fully connected world. And it is only a matter of time before one question will eventually arise. Are industries ready to adopt an IoT platform offered by operators? As far as we are aware, a number of industries are capable of E2E application establishment and are only in need of pipeline resources. For industries that approve of such an IoT platform, operators are forced to contemplate about another question: what should and should not be done? Specifically, operators must determine the best method to develop the industries' loyalty towards the enablement platform, stimulating the passion of partners, as well as demonstrating their value and control over the IoT platform.

1+N+X: Solution to Business Remodeling and ICT Value Mining

When examining the practices of world's leading operators in exploring the IoT market, one can easily ascertain that they have simultaneously traversed both two ends of the value chain (terminals and applications). This helps to fully probe the customer value in the ICT industry when conducting preliminary investigations into IoT business expansion. This is an effective outlet to cast off the stereotype of merely being a pipeline provider.

- 1: IaaS+ connection management platform (CMP), focusing on operator strengths (in most cases referring to infrastructure and connection management services).

- N: Device management (DM)/Application enablement platform (AEP), building an enablement platform together with partners.

- X: SaaS, supporting capability exposure and exploring ICT customer value.

1+N+X is a typical practice mode for operators.

In 1+N+X mode, the IaaS layer functions as the solid foundation, the CMP is the core, and the universal capabilities (device connection and management based on massive connectivity and concurrency) are supported by the PaaS layer. The enablement platform, SaaS applications, and industry applications are then developed in steps to promote the value of the entire IoT industry.

The traditional business model that involves network construction, subscription number allocation, and traffic-based sales is no longer suitable for IoT services. The setup of new business models is the key for operators to achieve successful IoT expansion for operators. According to the latest IBM statistics, approximately two thirds of IoT projects fail in the end and they implicate blame towards poorly selected business models.

II. Business Model Establishment: Three Out of Six (M1 to M6) Recommended Business Models

The value of the IoT industry chain components varies. The value of connections and platforms (middle parts of the chain) accounts for approximately 20%, whereas that of smart terminals and upper-layer applications (two ends of the chain) occupies approximately 60%. Industry data used in big data analytics can potentially create huge value.

Based on existing advantages, all players within the IoT ecosystem hope to secure a dominant position by expanding to upstream and downstream sectors. Business models in complex diversified forms are emerging and are undergoing continuous evolution. There are collectively six business models (M1 through M6, as shown in the following figure) for operators that will make their presence known throughout the entire industry chain. More services are involved from M1 up to M6. Operators can hope to achieve higher value in terms of additional services from the selected business models.

Figure 2: Six typical business models M1-M6 (source: Huawei Consulting)

M1 (IaaS mode) :

The IaaS mode is the simplest model, similar to the practice used in the traditional M2M market. Operators function as SIM card vendors, who are not aware of where and how the cards are utilized. In this model, operators are only responsible only for general network service provisioning and billing (involving mainly traffic package sales).

M2 (PaaS mode) :

In this model, operators establish a CMP for the IoT market to provide SIM card management services. Customers can use this platform to query and credit their accounts, activate and deactivate accounts in batches, and perform other related services. In this model, the primary source of income is generated based on traffic and messages.

In addition, operators can use the CMP that connects industry customers, to supplement cloud services with connection services and enter the module market.

<>>M3 (PaaS+ mode) :In this mode, the platform is the basis for all aspects. Platform economy features a bilateral or even multi-lateral market. The AEP in this model aggregates the CaaS capabilities (including voice, SMS, video call, and data storage) and third-party capabilities (including speech recognition/control, image recognition, and map). These capabilities can then be exposed to developers or industry customers through cloud APIs. The charging methods available in this model are based on traffic, messages, number of times APIs are invoked, and capability packages.

M4 (SaaS mode) :

M4 does not suit specific needs of various industries like M3. Alternatively, operators extract the common requirements of industries, based on which industry suites for universal use are developed. A small amount of customized development is required for the suite to be applied across diverse scenarios, such as smart homes, smart meters, and warehouse management. The available charging mechanism applicable in this model is based on the number of connected devices, or can be determined based on the suite as a whole.

M5 (SaaS+ mode) :

M5 is similar to M4, but offers additional value. In M5, operators not only provide upper-layer applications but also integrate upstream and downstream following an E2E approach. That is, operators offer connections, terminals, and an upper-layer application platform to participate in the industry's backend O&M through service provisioning. The benefits gained by these operators are largely dependent upon the potential value delivered to the industry. In certain cases, it is not unusual for operators to directly share a fixed portion of revenue. This model is applicable to small-scale and high-value new application scenarios that do not exclusively favor a particular type of industry.

M6 (BaaS mode) :

This model ranks the highest in regard to the engagement level of operators. Operators adopting this model obtain business licenses and participate in the crossover operations of the specific licensed industries.

M1, M2, and M3 are parallel business models. When adopting these models, operators do not need to offer differentiated products or services that cater to various industries. Instead, they benefit from standardized products at scale. When adopting M4, M5, or M6, operators will deeply delve into the vertical industries and extend from connections and platforms to each end of the industry chain. The higher the level of engagement, the more complex services become, and the higher the eventual return operators can receive.

Learning from the IoT practices of world's leading operators, Huawei recommends M2, M3, and M5. In these models, operators serve as a connection expert, platform provider, and solution integrator, respectively.

M2 connection expert:

Connections and cloud (IaaS) are the supporting pillars of this model, where basic cloud services can be packaged together. This addresses the industry needs for cloud services and increases service adherence, avoiding price wars and increasing the average revenue per connection (ARPC) value. SingTel is one of the leading operators that adopt this model, which is suitable for new IoT players possessing strengths in infrastructure networks but are still relatively inexperienced in IT service provisioning.

M3 platform provider:

It is a mainstream practice that the platform (PaaS) acts as the core for shortened TTM during enablement and integration procedures. Operator cloud, big data analytics, and other products can be merchandized in parallel to help support a very promising future. AT&T and Telefonica are leading operators that adopt M3. This is accomplished by offering open APIs to deliver a favorable IoT ecosystem (an operating environment, development tools, terminal management, data convergence processing, business analysis, and intelligent decision-making for industry developers). This model is suitable for operators with established ecosystem capabilities (in well-proven relationships with a large number of hardware vendors, software developers, and IT service providers).

M5 solution integrator:

An M5 adopter shares value with industries, while focusing on service integration (SaaS+ terminal). Operators using this model must be capable of delivering a full-package solution containing terminal devices, software apps, integration services, and other necessary components. This requires that the operators possess robust network and IT capabilities and have a deepened and comprehensive understanding of the target industries. However, in the current market only a limited number of operators that can measure up to this expectation, Vodafone and Deutsche Telekom being among them.

III. IoT Development Strategies from the Perspective of Business Models

The world's leading benchmark practice shows that operators usually tend to roll out their IoT business in three steps. The first step is connection service provisioning for vertical industries. A scale development foundation is laid based on connections. In the second step, operators provide platform services for willing enterprises with established IT capabilities to enable the industries based on the IoT platform. The final step allows operators to select between three to five industries to offer E2E solutions, which are further optimized during the application stages. These solutions can then be finalized and standardized for large-scale replication. The following figure shows the IoT business rollout for a selected number of operators.

Figure 3: Strategies for horizontal and vertical development of operators (source: Huawei consulting)

Operators are proficient in connection provisioning, but still have a long way to go towards realizing future success that relies on the platform. A high-performance IoT platform is warmly welcomed by industry developers during the initial stages of IoT development. They need an efficient platform to reduce development costs and shorten the TTM. Operators can only hope to win over industry developers with a cloud-based development platforms boasting low-cost IaaS (connection + cloud), open access management, and rich pre-integration capabilities. Only capable operators can assume a dominant role in building a formidable IoT ecosystem to gain access to the applications and massive data of the various industry partners.

How to leverage IoT platforms to aggregate ecosystem partners and discover high-value industries and applications in existing connections? The following three modes are available:

1) CMP + Industry enablement platform recruitment:

Operators focus on building a CMP, on top of which enablement platforms for multiple industries coexist. The DM/AEP for the industries can be jointly constructed and operated with partners, with a proportional share of revenue. For example, China Telecom works together with partners from public utilities, IoV and household appliances to build service enablement platforms together, based on the infrastructure, cloud services, and CMP. The IoV enablement platform built by China Telecom and their partners based on the IaaS and CMP provides PaaS for automobile manufacturers and post-installation users. This close cooperation with one another in the fields of business and market expansion helps to collaboratively explore the pre-installation and post-installation IoV markets. It is interesting to note that China telecom shares value with the IoV industry through proportional revenue sharing.

2) CMP + SI:

Operators establish the CMP, decouple the G-PaaS capabilities for multi-vendor co-construction, and zero in on the SaaS and integrated services. For example, Deutsche Telekom has launched the Multi-IoT Service Platform to attract platform vendors on the G-PaaS, including Huawei, Cisco, SAP, and Microsoft. The platform vendors build cloud PaaS capabilities that feature openness and universalization, and Deutsche Telekom focuses on integrated SaaS capabilities based on the PaaS platforms. In this way, Deutsche Telekom is able to provide quick enablement services, an IoT ecosystem, and even offer associated consulting services whenever needed.

3) CMP + SaaS centralized operation:

OneNET, the IoT company of China Mobile, developed a centralized method to manage the entire network after completing a thorough and comprehensive top down analysis of standardizing services. They then released brand-owned communications modules to extend to the downstream and through further cooperation was able to build an IoT platform (OneNET) for interconnection and offering industry applications in the upstream. The current shipment of their proprietary IoT modules has reached 1.5 million, and are widely applied in a multitude of other industries (such as energy, automobile, and consumer electronics).

IoT is a field that is perfectly set to prosper from operators' inherently advantageous resources. Pipeline provisioning is their continual pursuit. Market channeling, professional services, and user asset are intrinsic natural gifts. In the hopes of breaking away from the strict conventional label as a pipeline provider, operators must escape their confines of their current comfort zone and cultivate new capabilities to conquer the high-value campaigns ahead. Randall Stephenson, CEO of AT&T, said it best. "Adapt, or else!"